January 26, 2018.

- Fintech startups have better technology and ideas than banks, but they're also out to prove they're more transparent than the average bank in their products and their messaging

- Companies like Amazon offering service bundles like Prime are showing the world that people are willing to pay a fee up front in exchange for something valuable to them

Written by Tanaya Macheel,Michael Deleon,Guest Author - Originally published at this link.

If free checking accounts aren’t already a thing of the past, perhaps they should be, now that consumers are demonstrating that if something is valuable to them, they’ll pay for it.

Historically, banks have made most of their money on gotcha fees that can be crippling for low-value customers: overdraft fees, out-of-network ATM fees, fees for not maintaining a certain minimum balance. The lack of transparency around these extra charges only hurts their reputation for being companies that make money by taking money and it’s why it was so unsurprising when Bank of America announced this week that it’s yanking its free eBanking program and moving those customers to a standard checking account carrying a monthly $12 fee — which outraged the Twittersphere. Many people jumped to the defense of the bank’s poorer customers and ripped into the company for handing out bonuses at their expense (banks are used to this). There’s even a Change.org petition with at least 102,000 signatures opposing the move.

But banks have been reporting flat fee income for the past six quarters. Service charges on deposit accounts have hardly moved in several years and banks are changing their overdraft programs to improve customer relationships, which eats into that fee income. At the same time, companies like Amazon offering service bundles like Prime are showing the world that people are willing to pay a fee up front in exchange for something valuable to them. Fintech startups — which have better technology and cooler ideas than banks, but lack their resources and scale — are also showing customers they’re more transparent than your average financial institution both in their products and their messaging.

“It’s important to let consumers understand what you’re offering, what the fee structure is — and be abundantly clear about it — and then you can build trust,” said Jay Shah, CEO of Personal Capital. “That’s the name of the game in financial services; if you don’t have enduring trust you’re not going to win and keep customers.”

Incidentally, Bank of America has one of the most competitive mobile and digital banking offerings and no longer needs to give people an incentive to bank digitally instead of at branches (those were the terms of the account; those who wanted branch banking and paper statements paid an $8.95 monthly fee that was waived for customers who agreed to do all their banking digitally).

Great customer experiences and value propositions from the retail industry are forcing consumers to reevaluate whether they’re getting something valuable for what they’re paying and if the cost is worth it for something they can get from a fintech company or maybe one day a company like Amazon. The biggest change to the online lending industry since it first boomed is the increased customer expectation for transparency, according to Craig Schleicher, a senior manager in PwC’s consumer finance group.

“Transparency begets trust, but if you lead with something that says ‘zero fees’ and later that consumer unpacks that they were being taken to the cleaners and there was money being made in other forms, it undermines trust,” Shah said.

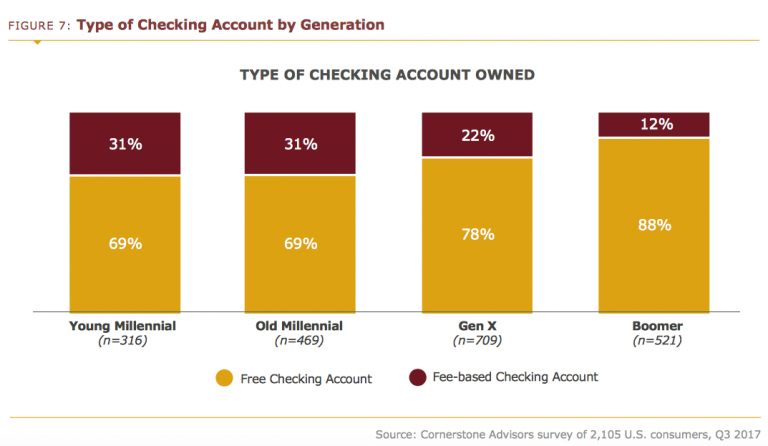

About 77 percent of people have a “free checking account” at their bank, according to a study from Cornerstone Advisors’ Ron Shevlin published last week. But nearly every free checking account holder paid at least one fee in the 12 months leading up to the survey. Out of 1,555 surveyed, 26 percent paid a third-party bank ATM fee and 25 percent paid an overdraft fee. They also paid fees to replace lost or misplaced ATM and debit cards, rush fees for those replacements, non-sufficient funds fees, wire transfer fees, international transaction fees, fees for overdraft protection and “extended overdrawn balances,” for stop payments and for statement copies, check copies and check image services.

“The issue isn’t wanting enhanced services for free, it’s the lack of transparency,” said one bank customer quoted in the report. “The $50-new-account offer advertised ‘free online banking’ but did not disclose the $7.95 per month ACH service fee on the offer itself. I don’t begrudge banks charging for their services; I do begrudge their lack of transparency.”

Almost 60 percent of people indicated they would consider switching accounts if their primary financial institution offered a hypothetical Amazon-like bundled checking account — which would include basic checking account services plus cell phone damage protection, ID theft protection, roadside assistance, travel insurance and product discounts — for a $5 to $10 monthly fee, Shevlin found. That’s the point of open banking that so many banks are missing: banks need to provide more than just financial products, they should provide any and all types of services for a customer’s entire financial experience, without necessarily owning all of it.

“If I’m a bank and I own that customer’s trust, why do I only sell her a mortgage?” said Simon Paris, deputy CEO of Finastra. “Why wouldn’t I sell her utility requirements, telephone, broadband, television requirements, moving-in services? Why wouldn’t I offer a platform-based service to her for the one of the most important events of her life?”

Financial services fees extend beyond basic checking accounts, and it’s not just the old guard pushing no fees and transparency. On Thursday, stock trading app Robinhood — which maintains that it doesn’t charge fees to open or maintain accounts, transfer funds or buy stocks — announced the launch of commission-free trading of 16 cryptocurrencies on its platform next month. The entire consumer value proposition of purchase financing startup Affirm has to do with transparency of its pricing, where instead of telling customers they can borrow $10,000 for their use at a 20 percent rate, it can lend $1,000 for something specific to be repaid in the near term at a rate that will in total cost the customer $1,117 by the time it’s paid off. Similar trends are taking place in the remittance space, according to Mike Landau, a payments analyst at PwC.

“There are a lot of new entrants that have these pricing models that don’t just charge you a fee,” he said. “They actually tell you the amount of money they make on just the transaction fee and what FX rate they provide to the sender, which is a practice that wasn’t always used by incumbents.”

Aspiration, a values based banking and investment startup, has responded to those kinds of bank practices by rolling out a checking account where the customers determine how much to pay for it. The company says it doesn’t take a cent from the fee, whatever the amount.

“The customer only pays us if they are so happy with what they’re getting they choose to pay,” said Aspiration CEO Andrei Cherny. “Banking services cost money. Employees and technology cost money. The problem is the model by which the banks are making that money, which instead of trying to make sure the customer is successful and happy often preys on those who can least afford the extremities.”

And Marcus by Goldman Sachs, the consumer personal loan startup within the old investment bank, has been pushing an anti-fee campaign since November scripted to show how frequently and commonly people accept fees without fully understanding why the fee structure is in place in the first place.

“Don’t Get Fee’d is a big part of our new campaign to create awareness,” said Dustin Cohn, Marcus’ chief marketing officer, at an event unveiling the campaign. “Once you understand personal loans can be a better option for you, [you see] many other lenders charge fees — origination fees, late fees, fees for paying down your loan early.”