November 29, 2016.

“You cannot see the picture if you’re in the frame.”

This old Chinese saying aptly summarizes the state of Fintech as seen through a “western frame.”

Having spent six months in the mystical land of Confucius, Dragons, Alibaba, Tencent, and Baidu — I have concluded that:

Written by Gaurav Sharma - Originally published at this link.

If there is a FinTech version of Silicon Valley — it is China. Period.

Today, there is no equivalent to China in the FinTech world. Here are some field notes with observations and insights from the region: —

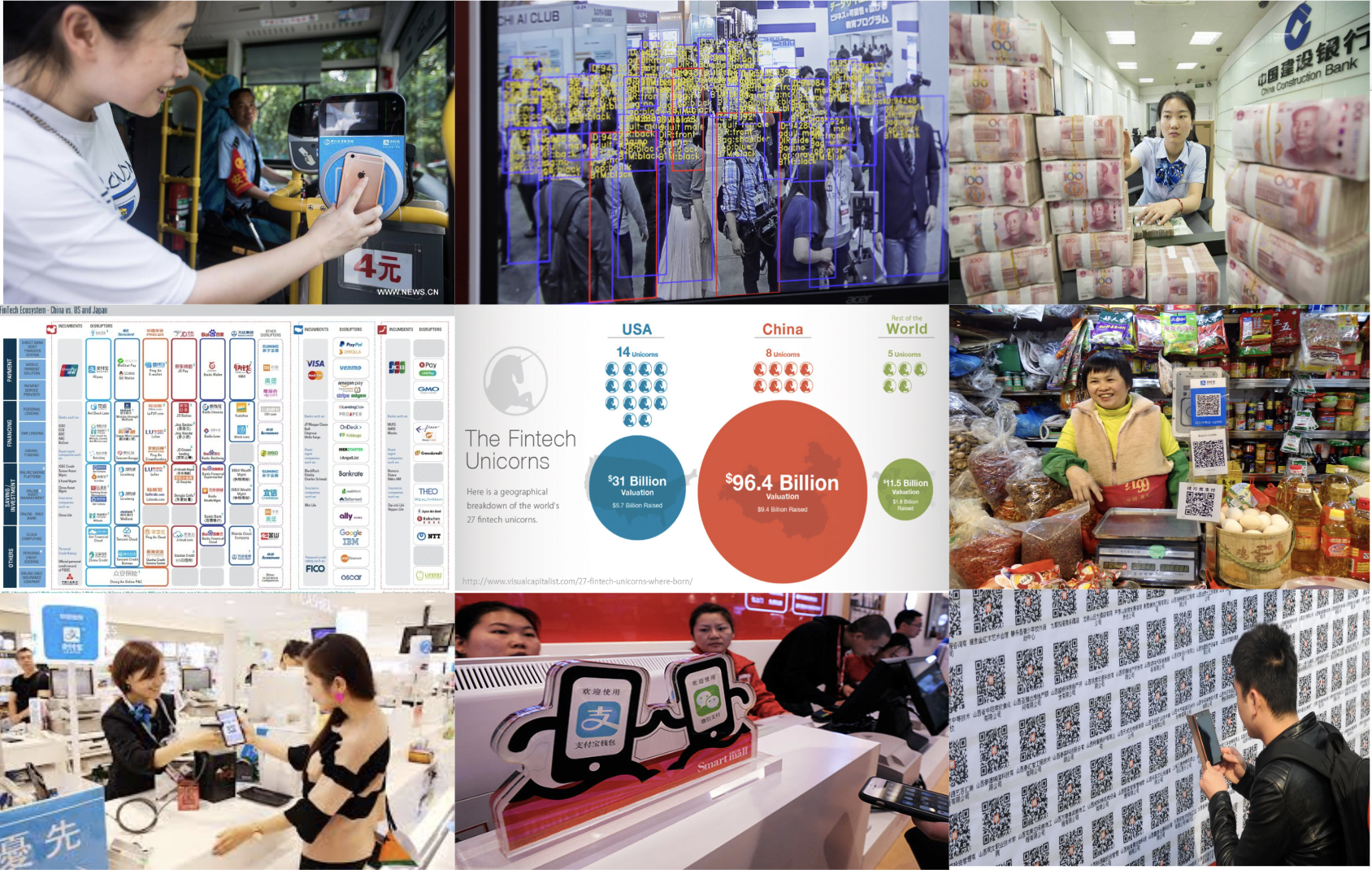

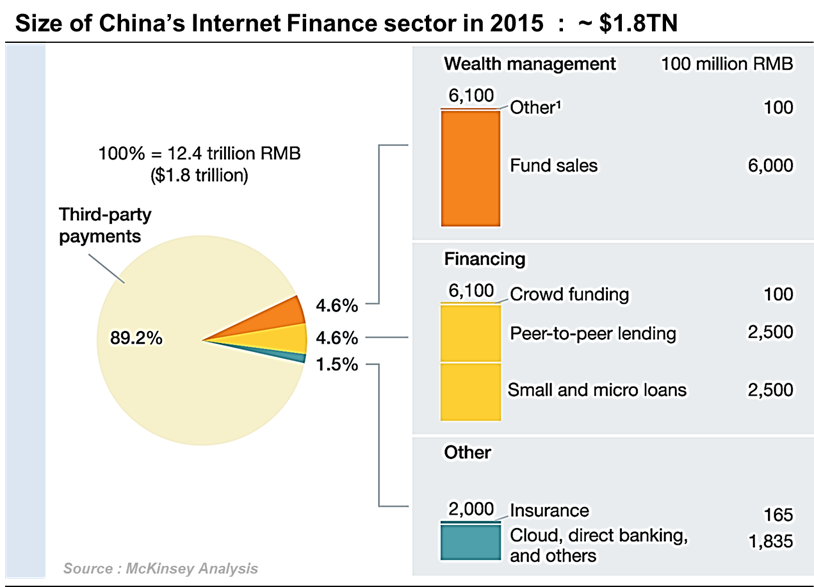

1. China is the world’s largest Fin-Tech market. In 2015, the market size of Internet finance in China was greater than $1.8 trillion.

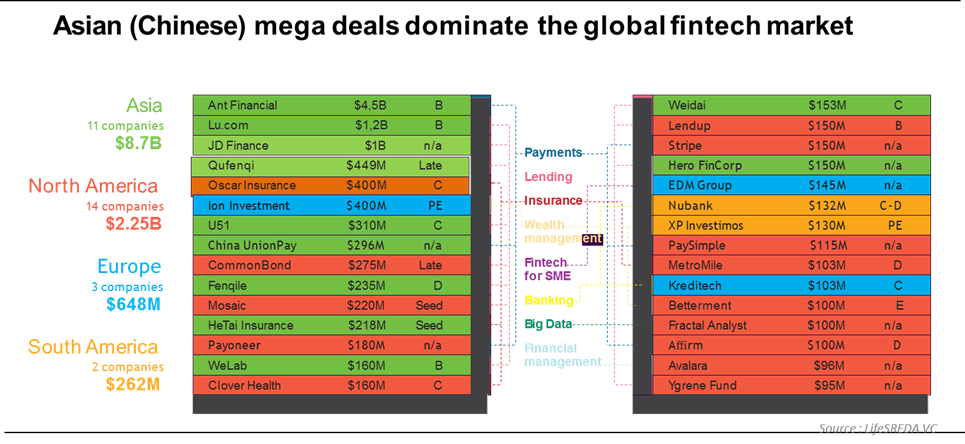

2. China is a global leader in every aspect. The country has taken in some of the largest chunks of global investment.

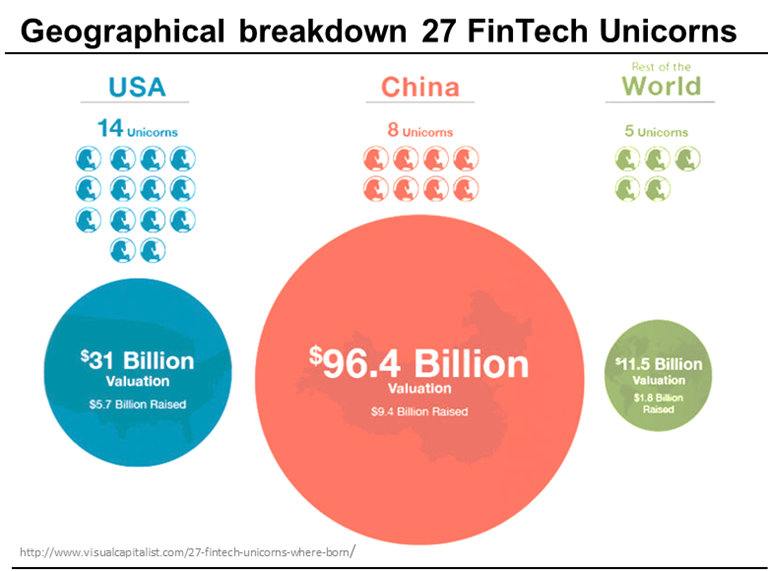

3. 1. Out of 27 FinTech unicorns, China’s 8 FinTech unicorns have raised $9.4 billion in funding and have a combined valuation of $96.4 billion.

4. China’s Internet ecosystem cannot be replicated. Factors contributing to its FinTech success include:

a. Rapid economic growth and a high national mobile internet penetration;

b. A large e-commerce ecosystem with domestic Internet companies focused on payments and access to a massive volume of transactions and user data;

c. Relatively ‘unsophisticated’ incumbent consumer banking sector;

d. Large underbanked and unbanked population and a high savings rate (30 %+);

e. More than $7 trillion of investable “retail” wealth earning very low interest;

f. Need for Credit -a financing gap of $3.5 trillion for small businesses and consumers; and

g. Accommodative regulations.

5. Chinese consumers have readily adopted FinTech services such as online banking, digital currencies, money transfers, payments, crowdfunding, lending, investments, and insurance.

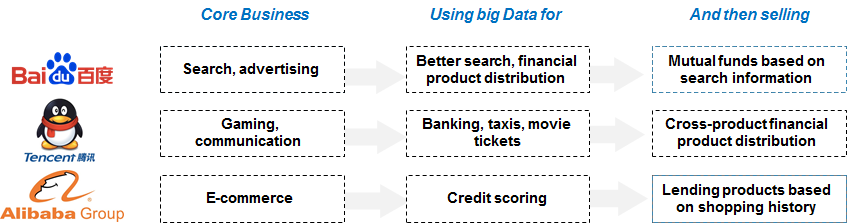

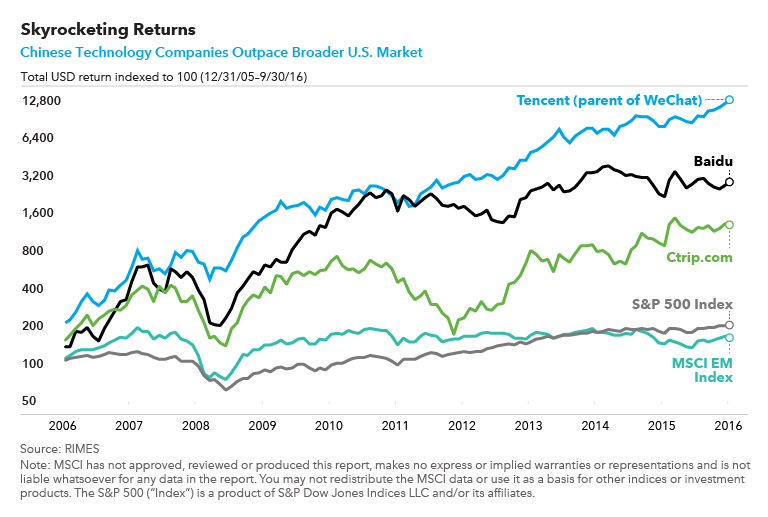

6. China’s dominance in technology is down to its Internet giants, also known as the BAT (Baidu, Alibaba, and Tencent); all three of them are at the core of the FinTech revolution. These three companies control e-commerce, messaging and search platforms and own several large FinTech businesses.

7. BAT companies enjoy extreme “unfair advantage” over incumbent banks and other players due to “proprietary rails & data (Payments, Commerce, transactions, and consumer).”

8. Since a majority of third-party payments and financial products run on ‘third-party rails’ — banks do not see or touch these transactions.

9. Alibaba, for example, has more than 500 million users who have provided the company with behavioral data for years. In comparison, National Credit Bureau, run by PBOC has data for only 300M people, i.e., less than 25% of the total population.

10. The four biggest FinTech unicorns in the world are from China: Ant Financial ($60B), Lufax ($18.5B), JD Finance ($7B), and Qufenqi ($5.9B).

11. The Chinese consumers did not inherit the web browsing habits of most Americans, and European customers, therefore, “Mobile is now the entry point for all customer acquisition strategies.”

12. Mobile payments transactions are at an all-time high, with more than 410 million people shopping online via their phones, as well as nearly 300 million people using their phones as a wallet for in-store payments.

13. The FinTech innovation in China is much more sophisticated than any other developed market. Tech and Platform companies with transaction data and proprietary rails are winning the game.

14. For large Internet companies, Financial Services has emerged as an ‘adjacent’ value category — sometimes bigger than the core business — by leveraging transaction data and communities.

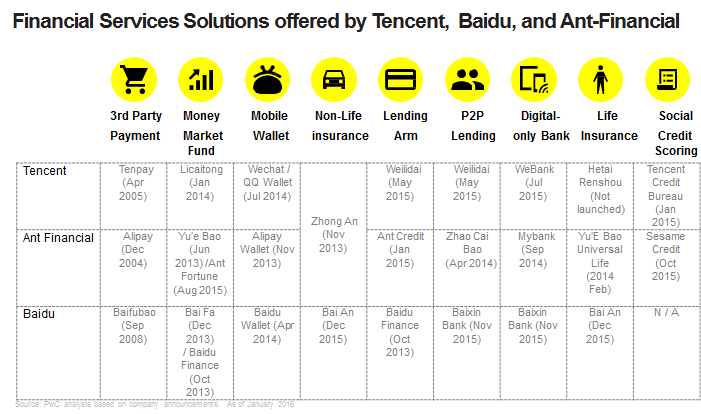

15. The triumvirate of China-“BAT companies”- are present everywhere — Payments, Lending, Banking, Insurance, and Investments.

16. China Internet giants dominate the FinTech space because they — got in on the ground floor when it came to building ‘e-commerce and payments’ ecosystems.

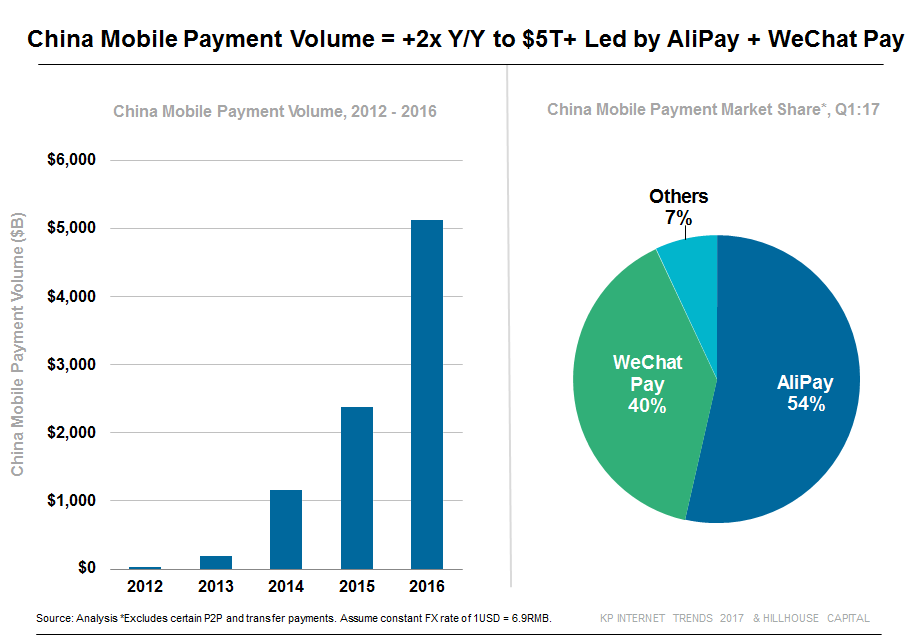

17. Alipay and Tencent — control about 90% of the Chinese mobile payments market. Payments are the foundation on which many other financial applications are built. Alibaba’s Alipay controls about half the market, and Tencent’s WeChatPay takes another 40%. (*updated)

18. Alipay and WeChat Pay are also used for point-of-sale (POS) payments.

19. Alipay and WeChat are ubiquitous in China. In 2015, Alipay processed~ 70% ($931B) of all mobile payments in the country and 3x as many transactions ($232 B) as PayPal did in 2015.

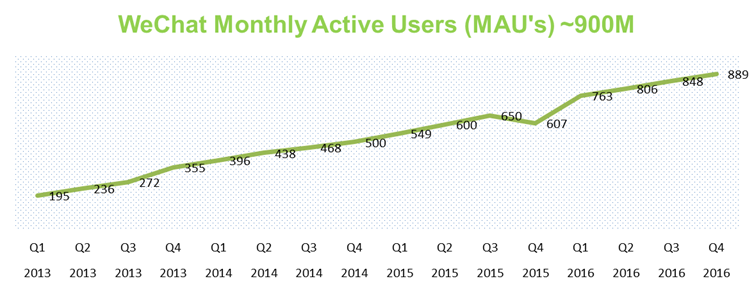

20. Over 1 billion people use Tencent’s various applications in Messaging, Gaming, Content, Payments and Wealth Management.

21. Wealth Management is another huge category. For e.g. Baidu’s mutual fund (RMB 3 billion) was sold out within three days of launch in 2014.

22. AntFinancial’s Yu’e Bao — in a short span of three years — is now the third-largest money market fund in the world with AUM ~$125bn. Another leading player is Tencent’s Licaitong.

#Alibaba now 3rd largest money market fund in the world with ~$120bn AUM , all in a span of 3 yrs. #Fintech #yuebao pic.twitter.com/vs71zr4q9M

— Gaurav Sharma (@Gaurav1105) May 27, 2016

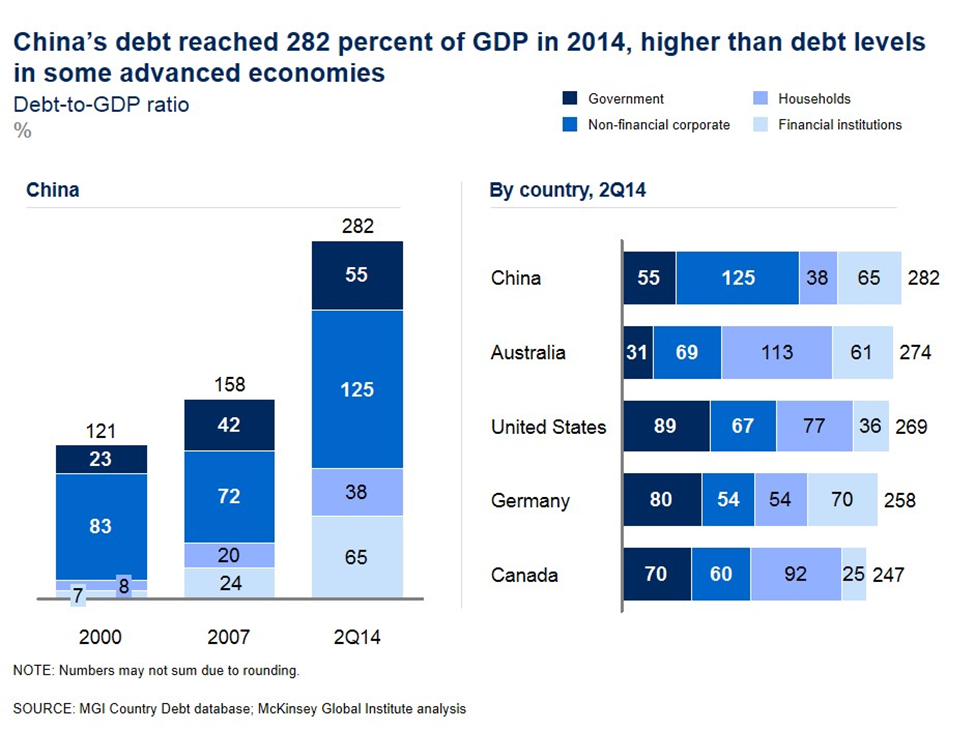

23. China’s growth story, since 2000, is fueled by massive “debt. “Excessive debt-leverage makes the entire ecosystem vulnerable to market shocks.

24. Competing in China is tough, and all the more hard if you have to compete against the BAT companies. Resultantly, domestic incumbent banks continue to struggle with their “relatively under-developed systems.”

25. China also has a very high savings rate (30 %+), so local banks have plenty of cash, but most of them do not have the systems and processes to do consumer lending profitably at scale.

26 The biggest FinTech startups are in Payments and Lending, which account for nearly 80% of the combined value of all unicorns.

27. Within “financing,” major segments of the value chain are Supply chain financing, Consumer financing, P2P lending, and Crowdfunding. Lufax is the largest P2P lender, with a valuation of $18.5 B.

28. Alipay’s mini-loans provider Hua-Bei (Just spend) is huge. It accounted for 26% of the transactions made on the singles day in 2016. Tencent lending application Wei Li Dai is by invitation only for Webank customers. Baidu also has a microloan provider focused on college students — You Qian Hua.

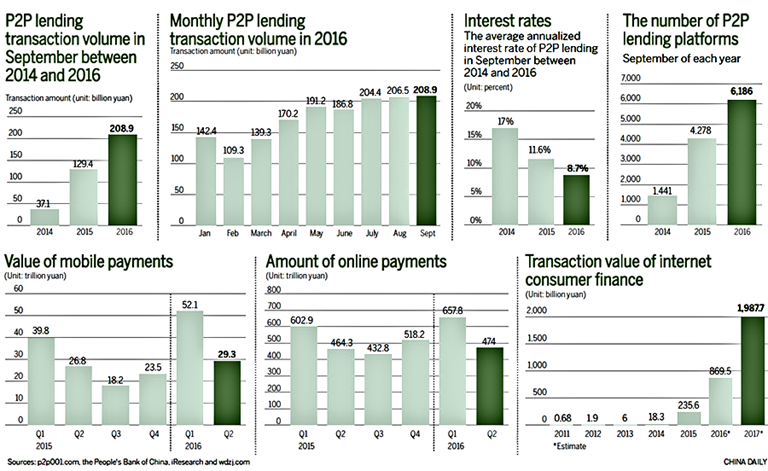

29. China has the highest number of P2P lending companies in the world. In 2015, registered P2P lenders originated approximately~ $60 B in Consumer loans &~$40 B in Business loans. However, the situation is far from rosy in p2p lending.

30. As of Jan 2016, there were 4500 P2P platforms in China with ~50% of them facing frauds, high delinquency, or liquidity-related issues.

31. The China Banking Regulatory Commission (“CBRC”) also came out with recent guidelines in August 2015.

32. Since then, there has been a nationwide crackdown on P2P lenders, and authorities are slamming brakes in the wake of financial scandals involving billions of Yuan.

33. As a result, weaker P2P platforms are shutting down. This wave of “cleansing and consolidation” is likely to continue over the next 12–18 months.

34. Although regulatory scrutiny is increasing, Chinese officials have been more liberal than regulators in other markets. The regulators are also looking at easing restrictions that currently hamper commercial banks’ investment into technology enterprises.

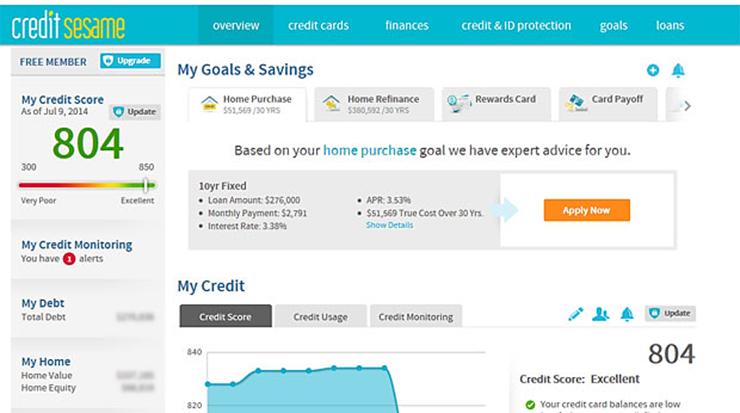

35. “Data is the New Gold,” and all the key internet finance companies are participating in this gold rush. Chinese FinTechs are using Big Data to provide credit scores to the “unscorable” For e.g Zhima Credit /Credit Sesame by AntFinancial. Tencent is also planning to start a credit-scoring business very soon.

36. 60% of the users have never owned a physical credit card. Traditional banks are not lending money to individuals because they lack a reliable credit scores.

37. The Chinese government is also developing a nationwide social credit system by collecting information online and providing all its citizens a score

38. China is redefining how the world thinks about payments. When comparing payments and lending solutions in the west, no contender offers the versatility and comprehensiveness of Alipay or WeChat Pay.

39. The market has mostly leap-frogged from cash straight to “mobile and digital.” and has well surpassed the “disruption point.”

40. Large payments companies are also beginning to position themselves for success “outside borders” through acquisitions, equity investments or strategic partnerships. For e.g AntFinancial’s recent investments in Thailand’s Ascend Money, and India’s PayTM, and their partnership with First Data in US and Ingenico in Europe.

41. Most of China’s 1 billion have no affiliation with a bank and will access financial services for the first time through an Internet company.

42. Until recently, China’s banking industry was 100% state-owned. Tencent’s WeBank(100% online bank),is first private sector bank in China.

43. WeBank was soon followed by the launch of Alibaba’s MyBank and Baidu’s Baixin Bank.

44. On the Insurance side, ZhongAn (one of the largest 100% online Chinese insurance companies) is backed by Alibaba and Tencent.

45. As the Chinese economy shifts from the “Ownership to Access” paradigm, the debt profile of the new generation is beginning to differ dramatically from the previous generation.

46. The technology sector now makes up for 30% of MSCI (China Investable Market Index). It was a mere 7% of the index three years ago.

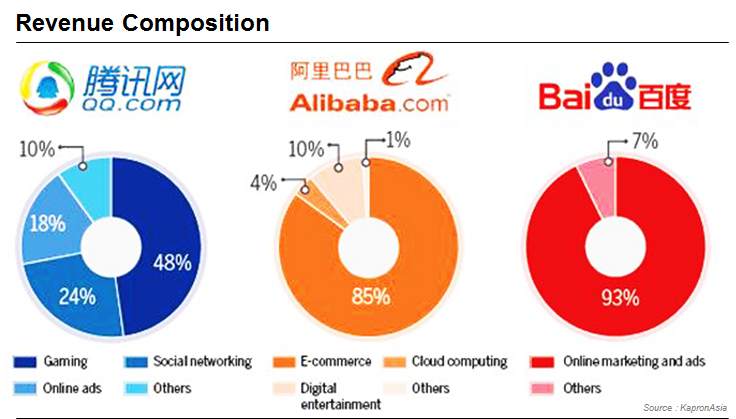

47. Together, Baidu, Alibaba and Tencent companies dominate China’s Internet ecosystem and generated $39 billion of revenue for the 12 months ending 30 June 2016.

48. For leading players- Speed and Scale is the core strategy. When it comes to FinTech, China is a world leader in every aspect. With the largest chunk of global investment in the sector, the market is adopting technology faster and at a scale bigger than anywhere else.

49. In a rapidly growing consumer economy, with more than 700+ million internet users, China FinTechs have fundamentally transformed the ecosystem and created immense wealth for all stakeholders.

50. That the Chinese have leapfrogged a generation of Consumer Finance is an understatement. No wonder, it is said that — “Saving and making people money” is the driving force behind many of the biggest consumer wins of the Internet era.

You can also follow this (below) tweet-thread for all things FinTech China.

“‘Why China is the FinTech Capital of the World?’— 50+ Points summary.” https://t.co/x3j9ppdjTH @Gaurav1105 pic.twitter.com/Mzf2MFkko1

— Gaurav Sharma (@Gaurav1105) November 29, 2016